An international merchant account is more than just a bank account; it’s a vital tool for modern online businesses. With the shift away from traditional payment methods like checks and cash, cards are becoming the go-to choice for consumers worldwide. Having an international merchant account isn’t just a smart move; it’s almost essential for tapping into global markets.

Running an e-commerce business nowadays that too without a merchant account is almost impossible. Therefore these international merchant accounts for cross-border payments make it easy to sell across borders and accept various payment types, including credit or debit cards. An international merchant account opens doors to a broader customer base and multiple currency options. Understanding its role can significantly benefit your online business in ways you might not have imagined.

An international merchant account is like a specialized bank account that lets businesses take payments from different countries. While it’s commonly used for handling eCheck, credit and debit card payments, ACH payments, wire transfers, or money orders, it can manage various payment methods. To set one up, you’d need to apply through a trusted merchant account provider.

These providers team up with banks to offer these accounts to businesses that want to process credit card transactions. Depending on the type of business you run, the bank will categorize your merchant account differently. Whether you’re accepting payments online, in-person, via a virtual terminal, or in another currency, there’s likely a merchant account option that fits your needs. Businesses in industries with higher risks often turn to these types of merchant accounts when they can’t find suitable services to send or receive international payments.

There are four main types of features fulfilled by a merchant account, and that is:

International payments play a crucial role in various aspects of global business:

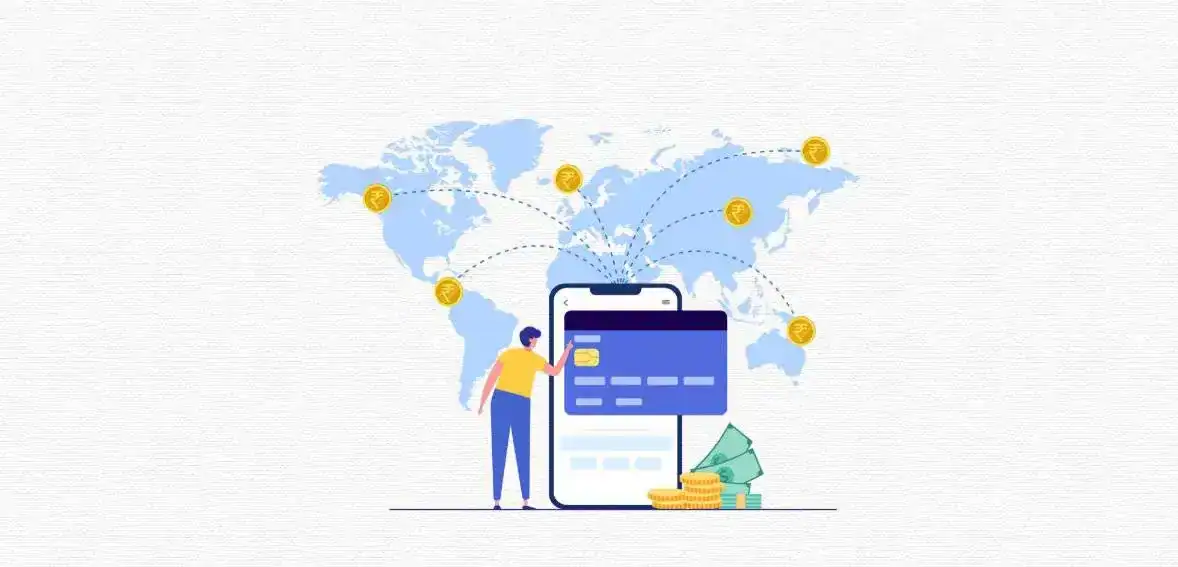

International payments, also called cross-border payments, happen when the person or business sending money is in one country and the recipient is in another. These types of payments are essential for businesses that work with international suppliers, workers, clients, or partners. Often, these payments involve converting money from one currency to another. Because these transactions cross country borders, you’ll typically face extra fees, like a markup for currency conversion.

International payments play a big role in global business. They make it possible for companies to trade across countries and grow beyond just their home market. These payments cover various business needs, like buying goods from foreign suppliers, paying international staff, or getting money from customers in other countries.

It might seem like handling money across borders is just a matter of dealing with beneficiaries in different countries, but it’s more complex than that:

One significant challenge arises from the lack of standardization in global payment systems. There’s a variety of payment methods and protocols worldwide, each with its unique characteristics and requirements. When money moves across these systems, it’s crucial to consider these differences. Trying to force one country’s payment system onto another often results in transactions getting declined.

Consider India, for example, credit card payments commonly use 2FA. This involves a PIN along with a one-time code sent via SMS or email. However, a similar transaction might not work with the same technology in countries like the USA. Similarly, CHAPS is a payment system in the UK that lets people send large amounts of money to others on the same day. While it’s mostly used for transfers within the UK, it can also handle some international transactions in either pounds or euros. Other payment systems from various countries include SEPA, CLS, Fedwire, and CIPS, among others.

Payment platforms need to handle these variations and be adaptable to changes in these systems over time. This adaptability is key to navigating the complexities of international transactions.

Transferring funds between countries can be tricky due to varying financial regulations and standards. Each country has its own rules, making it challenging to navigate the process smoothly. Some nations impose restrictions on the amount of money leaving the country and may demand extra documentation to verify the legitimacy of the transfer.

Additionally, the measures for risk mitigation and best practices, crucial for protecting companies against danger and fraud, differ across borders.

The challenge of international money transfers is further compounded by differences in currencies. Exchange rates come into play, requiring the conversion of the sender’s currency to that of the recipient.

This process may incur extra fees and, at times, unfavorable exchange rates. Payment orchestration platforms play a critical role in ensuring accurate calculations of exchange rates and transparent disclosure of fees to customers.

One of the significant advantages for your global business is the assurance of timely payments. Late payments from international customers can create cash flow challenges and hinder your business growth.

With an international merchant account, you can count on prompt payments. These accounts offer various ways for your global customers to make payments securely. Plus, you can quickly verify the availability of funds.

With an international merchant account, you won’t need to constantly follow up with customers to confirm payments. This streamlined process not only makes transactions smoother for buyers but also ensures you receive payments faster, benefiting your business operations.

To enhance your global online sales and save money, it’s wise to use a payment platform connected to banks in the regions where your customers are located.

A savvy approach for global e-commerce success is setting up international merchant accounts in key regions you serve. For instance, handle US transactions with a US bank and European sales through an EU bank. These banks are all linked to one central payment platform, making management straightforward.

Additionally, countries often have their own preferred payment methods. With international merchant accounts, you can easily offer these local payment options through your payment gateway, catering to diverse customer preferences and potentially increasing sales.

Running an online store comes with the risk of encountering fraudsters who pretend to be genuine customers. Regardless of the size of your e-commerce business, you’ll likely face challenges like unauthorized payments and disputes over chargebacks. These issues can harm not only your business’s financial health but also its reputation.

International merchant accounts offer more than just a way to accept credit and debit card payments online. They come with built-in features to help combat fraud and protect your business. With specialized payment gateways and processors, these accounts are designed to detect and prevent scams like bounced checks and other online fraud schemes.

With the help of these accounts, you can accept online payments with greater confidence, minimizing the risks associated with fraudulent activities. These accounts maintain comprehensive records of all online transactions, making it easier to resolve any disputes, such as chargebacks from problematic customers. Most importantly, this added layer of security helps safeguard your business’s reputation and credit rating. In short, opting for an international merchant account can provide a secure and reliable way to handle payments and transactions for your business.

International merchant accounts help businesses and customers avoid surprise fees during payments. If you’re dealing with large payments or many international transactions, you might be paying extra fees without even realizing it. Webpays offers a solution for businesses needing high-risk merchant transactions.

Often, fees for incoming wire transfers aren’t clear until the money arrives. This lack of transparency can lead to unexpected costs. With an international merchant account, you can either reduce or completely avoid these bank fees.

Having an international merchant account gives you peace of mind when it comes to online transactions. You won’t have to worry about hidden fees or other obstacles that could affect your access to funds. These accounts simplify the process by handling direct debit and ACH transactions without the need for expensive global wires. Some even eliminate flat fees for deposits into your account, making it easier and more cost-effective to accept payments.

International merchant accounts are key in helping businesses thrive in today’s interconnected market. These specialized accounts make cross-border transactions easier by offering features such as currency conversion, risk management, and multi-currency handling.

They ensure payments boost e-commerce sales and protect against fraud–all that in affordable fees. With an international merchant account, businesses can streamline operations, build trust with customers, and gain an edge in the global market. These accounts pave the way for transactions and sustainable growth on a global scale.

An international merchant account is a specialized bank account that empowers businesses to accept various forms of payment. While it’s commonly used for handling credit card and eCheck transactions, it can accommodate other payment methods as well.

Cross-border payments can take several forms, including: Wire transfers Bank transfers Electronic transfers Debit cards Credit cards Prepaid card (debit and credit) ACH transactions

When it comes to international sales, wire transfers, and credit cards often emerge as preferred upfront payment options for exporters.

Offering multi-currency processing is vital for maximizing profits from global customers. Simplifying the buying process by presenting prices in familiar currencies reduces confusion, keeping potential buyers engaged and less likely to navigate away from competitors.

Obtaining an international merchant account is typically a straightforward endeavor. You’ll need to submit an application and provide essential business documents such as identification for the authorized account user, a voided check for settlement accounts, recent business bank statements, payment processing history, and information about your business entity.